Last updatedJune 2026

Top No Medical Exam Life Insurance Ohio 2026

Get insured online, no medical exam needed

You can protect your family with one of these top term life insurance companies without taking a medical exam.

You can protect your family with one of these top term life insurance companies without taking a medical exam.

No medical exam life insurance lets you apply for coverage without undergoing a physical exam or lab work. Instead, insurers evaluate your health using questionnaires, prescription history, medical records, and other digital data sources.

For you, this means faster decisions, less friction, and fewer steps. This is especially useful if you want coverage quickly or prefer a simpler application process. The trade-off is that insurers are taking on more uncertainty, which often results in higher premiums or lower death benefits compared to fully underwritten policies.

You answer a short set of health questions, but no exam is required. Approval usually takes a few days, and coverage limits are moderate.

Why this matters: This is often the best balance between speed, cost, and coverage if you’re in average health.

Insurers use digital records, like prescriptions, medical history, and lifestyle data, to make quick decisions, sometimes within 24-48 hours.

Why this matters: If your records are clean, you may qualify for pricing close to traditional policies without an exam.

No health questions and no exam, but coverage limits are low, and premiums are higher. Many policies include a graded or waiting-period benefit.

Why this matters: This option exists primarily for people who can’t qualify for other types of life insurance and need final-expense coverage.

| Free online quote |

"Foregoing a traditional medical exam doesn't give you a free pass. Life insurance companies still take a close look at your medical history using the Medical Information Bureau (MIB). Plus, it's easy to uncover health patterns in your pharmacy records based on the prescriptions you fill.”

Life insurance without a medical exam typically costs more than traditional life insurance because the insurer has less medical information upfront. Your actual cost depends on:

For younger or healthier applicants, accelerated underwriting policies can narrow the price gap, and coverage may be cheaper than you think. For older applicants or those with health conditions, simplified or guaranteed acceptance policies may be the only option, but at a higher monthly cost.

"Life insurance shoppers often believe that skipping a medical exam will result in a very high premium. While many no-exam policies do have higher rates, healthy people often find the rates to be competitive with fully underwritten policies. Ultimately, it's important to compare policies and premiums to find the best rate."

To choose the best no-exam life insurance, focus on the policy that gives you enough coverage at a price you can sustain long-term, not just the one that approves you fastest. The right choice balances coverage amount, underwriting type, total cost, and insurer reliability—based on your health, timeline, and financial goals.

| Apply 100% online in 5 min |

| Company | Application Type | Coverage Options | Underwriting Approach | Digital Experience |

|---|---|---|---|---|

| Banner Life & William Penn | Online & assisted | Term life | Accelerated underwriting | Moderate |

| Ladder | Fully online | Term life | Accelerated underwriting | High |

| SelectQuote | Agent-assisted | Term & final expense | Simplified & guaranteed | Moderate |

| SoFi | Online | Term life | Accelerated underwriting | High |

| Ethos | Fully online | Term & whole life | Simplified & accelerated | High |

| Fabric by Gerber Life | Online | Term life | Simplified issue | High |

| Progressive Life Insurance | Assisted | Term & permanent | Simplified issue | Moderate |

| Fidelity Life | Online & assisted | Term & final expense | Simplified & guaranteed | Moderate |

No-exam life insurance is best suited for people who value speed, simplicity, or access over getting the absolute lowest premium. It’s often a situational solution rather than a one-size-fits-all policy.

You may want to consider it if you:

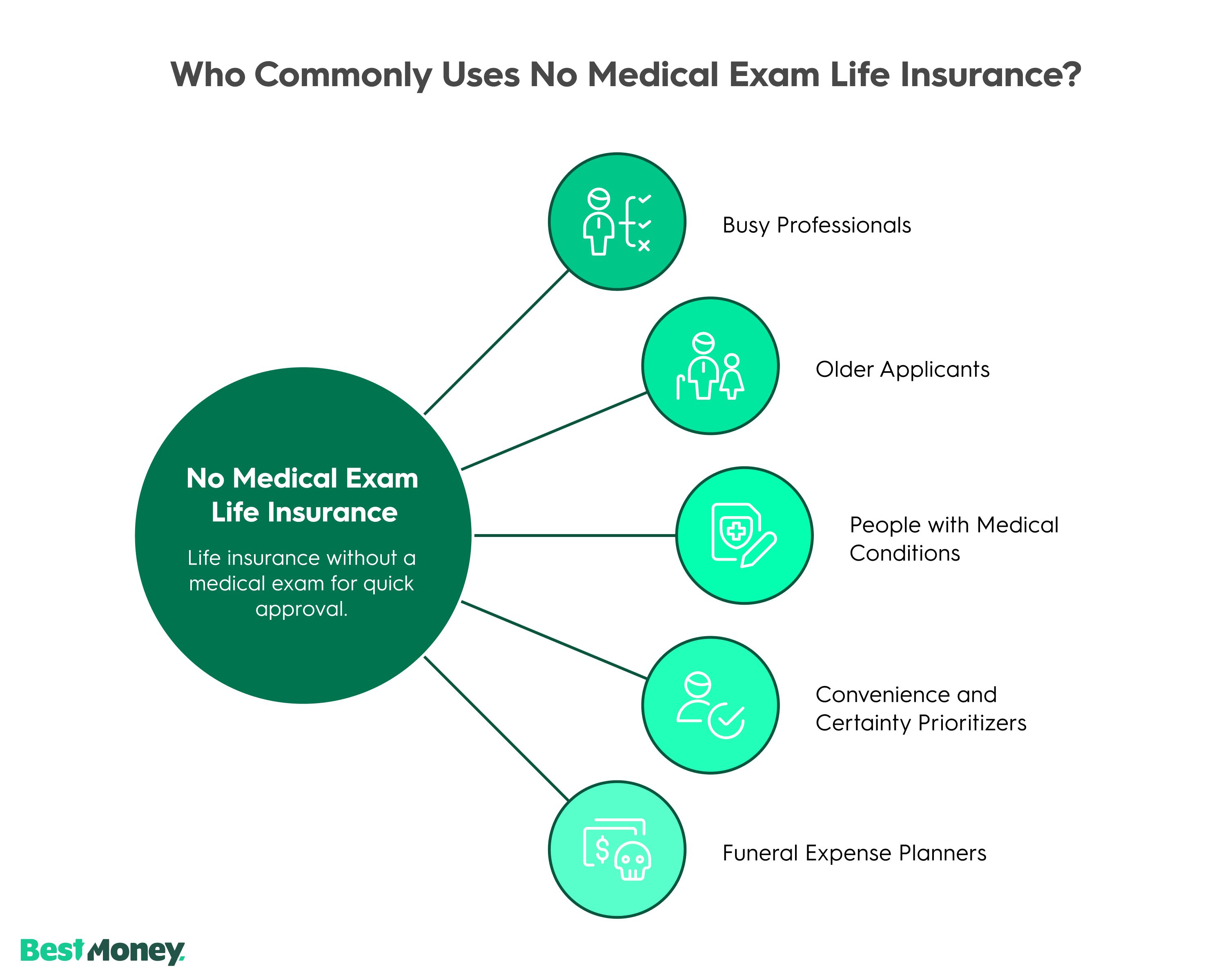

It's commonly used by:

If you're healthy, flexible on timing, and focused on long-term cost efficiency, a fully underwritten policy may be a better fit. But when speed, ease, or eligibility is the priority, no-exam life insurance fills an important gap.

| Personalized term life insurance quotes |

Based on Reddit discussions, many applicants value no-exam life insurance for its speed and reduced stress during the application process. Users frequently mention that policies can be surprisingly comprehensive, especially through accelerated underwriting, but also warn that pricing and coverage limits vary widely depending on health, age, and insurance company.

Common themes include the importance of comparing providers, watching for waiting periods on guaranteed acceptance policies, and using brokers or comparison platforms to avoid overpaying.

Overall, community sentiment highlights convenience as the biggest win, and cost awareness as the biggest caution.

At BestMoney.com, we understand the importance of making informed financial decisions. Our team of financial experts and editors conducts thorough research across lending, banking, home loans, personal finance, and insurance to provide you with comprehensive comparisons and insights. We continuously update our content to reflect the latest market trends and offerings, ensuring you have access to current, reliable information.

We offer a wide range of services including detailed comparison tools and expert reviews, all designed to meet your specific financial needs. Our mission is to empower you to make confident, well-informed choices that help you achieve your financial goals.

BestMoney evaluates no-exam life insurance providers by combining policy analysis with real-world consumer considerations. The goal is to identify options that balance cost, accessibility, and long-term reliability, not just fast approval.

Our evaluation includes:

This approach helps surface providers that perform well not just on paper, but in practical, everyday use.

No medical exam life insurance uses digital underwriting instead of a physical exam. You answer health questions, and the insurer reviews prescription history, medical records, and third-party data to assess risk. Approval can take minutes to days, and coverage starts after issuance and first payment. Premiums are typically higher due to limited medical screening.

It can be worth it if speed, convenience, or eligibility is your priority. It’s ideal when you need coverage quickly or want to avoid medical testing. However, if you’re healthy and can wait, traditional policies usually offer lower premiums and better long-term value.

No-exam life insurance is best for people who value fast approval and a simple application. It’s commonly chosen by busy professionals, older applicants seeking final-expense coverage, or individuals with health conditions that may complicate traditional underwriting.

No-exam life insurance usually costs more than traditional policies because insurers rely on limited medical data. Your rate depends on age, gender, health history, coverage amount, and policy type. Accelerated underwriting may offer rates closer to fully underwritten policies if you’re in good health.

Common types include simplified issue (health questions, no exam), accelerated underwriting (digital data review with faster approval), and guaranteed acceptance (no health questions but higher premiums and lower coverage limits). The best option depends on your health and coverage needs.

| | Get a free quote |

Best for: Traditional carriers offering no-exam pathways

Banner Life & William Penn offers up to $5 million in no-exam term life insurance to eligible applicants between the ages of 20 and 60. Policies that use lab-free underwriting (accelerated) get approved in as little as 10 days.

Pros

Cons

Why we chose it: Banner Life / William Penn is a reputable life insurance company that offers no-exam coverage with generous policy limits in all 50 states.

| | Apply 100% online |

Best for: Fully digital term life with flexible coverage management

Ladder offers no-medical-exam term life insurance with up to $3 million in coverage. You have the option to increase or decrease your policy limit if your family’s financial needs change. Many applicants can get coverage on the same day they apply.

Pros

Cons

No permanent life insurance options.

Doesn’t sell riders.

Why we chose it: Ladder is a digital life insurance company that offers no-exam term life with instant decisions, and flexible coverage if you need to raise or lower your policy limit.

| | Personalized insurance quotes |

Best for: Comparing no-exam policies from multiple insurers

SelectQuote is an independent insurance brokerage that helps shoppers compare no-exam life insurance options from multiple top-rated carriers. Through its licensed agents, applicants can explore term and permanent coverage options that may not require a medical exam, depending on eligibility. The company provides guided support throughout the application process to help match consumers with coverage that fits their needs and budget.

Pros

Cons

Must apply through an agent rather than a fully self-serve online process

Policy availability and underwriting requirements vary by carrier

Why we chose it: SelectQuote makes it easier to shop and compare no-exam life insurance from several insurers in one place, with agent guidance to help simplify the process.

Disclaimers

AM Best Rating: *A.M. Best's Financial Strength Rating (FSR) is a measure of an insurer's financial strength and ability to pay out claims to policyholders. An "A" rating with A.M. Best indicates that an insurer is considered to be top of the industry in ability to meet ongoing insurance obligations.

*Ethos: Life insurance without an exam requires a few online health questions.

*Ladder: Just answer some health & lifestyle questions

¹Eligibility for Progressive Life Insurance depends on age, health, and additional underwriting factors. The exact policy type, coverage amount, and term length offered will vary.

Ladder Insurance Services, LLC (CA license # OK22568; AR license # 3000140372) distributes term life insurance products issued by multiple insurers – for further details see ladderlife.com. All insurance products are governed by the terms set forth in the applicable insurance policy. Each insurer has financial responsibility for its own products. Submission number 260421-5417080