Last updatedMarch 2026

Travel insurance for your trip

Explore with peace of mind

Find the best travel insurance to stay covered wherever you go. Compare the best travel insurance companies and choose one that suits your needs.

Find the best travel insurance to stay covered wherever you go. Compare the best travel insurance companies and choose one that suits your needs.

Faye Travel Insurance is a new travel insurance provider, underwritten by United States Fire Insurance Company. It was built during the COVID-19 pandemic and launched in early 2022.

Claims processing is quick, and you can do this on Faye’s mobile app. The company offers fully customized plans to ensure you're not paying for features you don't need. What’s more, its 24-hour customer support means you can speak to real people (not robots!) throughout your travels.

Faye is a modern take on travel insurance. It’s a fully digital experience that allows you to purchase policies, file claims, and receive payouts through an app. The entire process is fast and secure, and you can receive reimbursement directly to your Faye Wallet, a secure digital debit card that you can add to Apple Wallet or Google Wallet, to then simply tap and pay.

Faye's tech-based approach makes it suitable for people who want something different from lengthy paperwork-based traditional insurance. It’s also ideal for frequent travelers who value convenience and want a plan that fits their exact needs. With Faye, you start with a base plan that you can customize with additional bundles, including rental car care, extreme sports protection, vacation rental damage protection, and “cancel for any reason” coverage.

Unlike other travel insurance providers, Faye doesn’t offer tiered plans. Instead, there is one base plan with the option to add additional riders such as pets, extreme sports, and medical coverage. The base package includes the following:

| Base plan | ||

|---|---|---|

|

| Maximum payout limit |

Medical cover | Medical evacuation and repatriation of remains benefit | Up to $500,000 |

Return transportation | Included | |

Transportation of child/children | Included | |

Transportation to join you | Included | |

Political or security evacuation and optional natural disaster evacuation | Up to $100,000 (international trips only) | |

Accident and sickness medical expense | Up to $250,000 for international trips ($50,000 for domestic) | |

Dental expense sublimit | Up to $750 | |

Cancellation and interruption | Trip cancellation | 100% of trip cost |

Trip interruption | 150% of trip cost | |

Trip delay | $300 per day, to a maximum of $4,500 | |

Travel inconvenience* | Baggage delay | $200 |

Delay at security check-in | $200 | |

Flight delay | $200 | |

Flight cancellation | $200 | |

Flight diversion | $200 | |

Rental property lockout | $200 | |

Hotel late arrival | $200 | |

Travel delay: internet usage fee | $50 | |

Travel delay: airline club admission fee | $25 | |

Baggage and personal effects** (Up to $2,000 per person per trip) | Baggage delay | $300 |

Passport, visa, or other travel documents replacement | $50 | |

Credit card charges and interest | $50 | |

Per article limit | $150 | |

Combined articles limit | $200 |

*Travel inconvenience: up to a maximum of $600

**Baggage and personal effects: up to a maximum of $750

For an additional cost, you can include “cancel for any reason’” coverage. You can also pay extra for adventure and extreme sports protection within your medical cover. Faye offers additional bundles for rental car protection and pet expenses, the details of which are below.

| Rental car bundle | |

|---|---|

Optional rental car damage and theft coverage | Up to $50,000 |

Optional travel inconvenience: Closed attractionsBeach closureRainy vacationRental vehicle breakdownCredit/debit card canceledVacation rental | $200 per inconvenience, up to a maximum of $600 |

| Pet parent bundle | |

|---|---|

Optional pet or service animal return | Up to $250 |

Optional pet kennel | Up to $250 |

Optional pet or service animal travel medical expense | Up to $2,500 |

Optional quarantine kenneling expense | Up to $2,500 |

The cost of your policy depends on your trip details and the state in which you live. Most international destinations cost a similar amount, and the duration of your trip does not usually impact the base plan cost. However, it will likely increase your estimated trip cost—which will increase the price.

I inquired about insurance for a two-week vacation in Italy for a Colorado resident. My trip insurance cost $114.50 for the base plan, based on an estimated trip cost of $1,000. The trip cost is the maximum amount Faye will reimburse me if my trip is canceled. For a trip costing $4,000, the base plan cost is $211.82. These figures are accurate as of March 2023.

I also had the option to include extras on top of my base plan. “Cancel for any reason” coverage costs an additional $20.35, and adventure and extreme sports protection costs $37.86. If I wanted to protect a rental car against accidental damage and theft, this would add $7.58 per day. Vacation rental cover comes to $17.04, and pet care adds another $25.36. The total policy cost for the same trip is now $338.81.

You can purchase Faye’s travel insurance directly through its website or mobile app. The process is designed to be as quick and straightforward as possible, with one comprehensive base plan and the option to purchase additional insurance bundles.

If you need to submit a claim, you can do it via the Faye mobile app or by email. You can use your app to keep track of the claim status and to see if it has been approved. If you qualify for a quick reimbursement, Faye will send money to your Faye Wallet, which you can access immediately. The app also allows you to transfer that money directly to your bank account. Faye aims to process all claims within 48 hours.

Faye also offers real-time travel updates and 24/7 customer service via the app. You can be notified of flight delays, gate changes, and other helpful information like which baggage carousel to go to when you arrive. Its customer service team is available to offer guidance and help with time-sensitive tasks, like finding an emergency doctor.

To get started, select the "Check Pricing" button on Faye’s website. You’ll need to provide details about your destination, your home address, the number of people traveling, and each traveler's name and date of birth.

You’re then taken to a policy details page which will outline what’s covered and options for additional protection, such as rental car cover and pet care. Once you’ve tailored your cover to your requirements, select the “Get Covered” button.

You can now pay via Google Pay or enter your card details to purchase your policy. After you’ve paid, Faye will send you an email containing the policy information.

You can also follow the same steps on Faye’s mobile app. Via the app you can also pay with Apple Pay. I found the process straightforward and quick, both online and via the app. The steps are easy to follow, and the information provided on the policy details page is clear and transparent.

Faye doesn't charge any administrative, arrangement, or amendment fees on its insurance products. If you cancel your travel insurance before starting your trip, you can receive a full refund up to 14 days after buying the coverage, as long as you haven’t already made a claim and as long as your trip hasn't started yet. Faye’s terms are set out in its Terms of Use document, available to read before you commit to purchasing.

Yes! Faye is a tech-driven app-based service and doesn’t just include an app as an afterthought like many insurance companies. The app is available for both Android and iOS, and you can use it to complete the whole process from initial pricing inquiry to making a claim.

Some of the most highly-praised features of the app include its 24/7 customer support chat. You’ll also get real-time travel alerts direct to your phone, for example, if your flight is delayed. What’s more, the app includes the Faye Wallet, a secure digital debit card that ensures fast reimbursement on claims and common travel inconveniences, like flight delays. It works with Apple or Google Pay, or you can transfer the funds to your bank account by tapping "Redeem" in the wallet.

Despite being a newcomer in the travel insurance industry, Faye has gained a good reputation among its customers and has an excellent score of 4.7 on Trustpilot. Multiple customer reviews praise its reliable customer service, user-friendly mobile app, and prompt notifications of flight delays and reimbursements.

Faye is a member of the United States Travel Insurance Association (USTIA), and its travel insurance coverages are underwritten by the United States Fire Insurance Company.

Faye prides itself on its excellent customer service. Its website and mobile app have a chat feature, and you’ll be able to talk to a real human rather than a robot. I used the chat function to ask Faye a question and got a friendly and informative response from one of its support team within a few minutes.

You can also contact Faye via phone on 833-240-7056 or email them at support@withfaye.com. The chat function, email queries, and phone lines are all staffed 24 hours a day, seven days a week. Phone calls are answered within five minutes and emails are responded to within 24 hours.

Faye’s website has a FAQs section and a blog, and you can also sign up for its newsletter and receive announcements, updates, and travel inspiration in your inbox.

Faye is a new player in the travel insurance market, aiming to revolutionize the industry, and my experience with the company has been very positive. Its friendly and helpful 24/7 customer service is available through the website and mobile app and ensured I was able to get my questions answered when I needed them.

The app also comes with features like real-time travel alerts and digital payment cards, which sets it apart from its competitors. The base plan and extra bundles cost less than many other insurers, making Faye a great choice for budget-conscious travelers.

Is Faye Travel Insurance legit?

Yes, Faye is a legitimate travel insurance company. It provides cover for medical expenses, trip cancellation and interruption, and other travel-related losses in accordance with its policy terms.

Is there a money-back guarantee?

Faye does not offer any money-back guarantees. However, it does offer a 100% refund if you cancel your policy within 14 days of purchase and have not made a claim.

What is the Faye Wallet?

The Faye Wallet is a digital payment card in the Faye app that allows quick reimbursement when making a claim. It works with Apple or Google Pay, or you can transfer the funds to your regular bank account by tapping “Redeem” in the wallet.

Emma Street is a finance writer at BestMoney.com specializing in debt consolidation and loans. With a BSc in Computer Science and over 15 years in software development, her experience in InsureTech and FinTech fuels her passion for exploring the intersection of technology and personal finance.

TravelInsurance.com has been helping customers compare and purchase travel insurance policies for over 10 years. It’s owned and operated by DigiVentures Holdings, LLC, which is fully licensed. What’s more, it only works with top-rated, leading travel insurance partners.

TravelInsurance.com offers insurance policies from various partners that are tailored exactly to your requirements. You can customize your policy for extra or specialized cover, and annual travel insurance is available. I found it very easy to use, and I was impressed with the options TravelInsurance.com presented.

If you’ve ever tried to purchase travel insurance, you’ll know it can be hard to figure out what sort of policy you should get and from which provider. TravelInsurance.com aims to simplify this process by recommending policies that are personalized for your needs.

You begin by entering information about your trip and requesting a quote. You’ll then see a selection of policies with varying features and coverage levels, which you can select and purchase immediately.

This convenience is one of TravelInsurance.com’s standout features. It offers some of the lowest prices around, and it enables you to purchase coverage in minutes. The customer service team is on hand to help you if you have any questions, and I found the entire experience of using it to be quite pleasant.

TravelInsurance.com is suitable for anyone who’s struggling to find the right travel insurance policy. It enables you to purchase a policy for your trip in minutes, and it’s super easy to use. What’s more, it has very competitive prices, and there’s everything from single-trip insurance to annual coverage.

TravelInsurance.com is a comparison website that doesn’t offer its own insurance plans but instead works with various industry partners. Because of this, there are significant differences in what’s included in each policy. The exact features you get will depend on the partner you choose.

Some offer basic coverage for trip cancellation or interruption, and stolen or lost baggage. Others include more specialized coverage, including flight accident, emergency medical, and medical evacuation.

TravelInsurance.com’s partners offer a wide range of policies at different price points. The cost of a single-trip plan will vary according to your destination, the cost of your trip, and the duration of your holiday.

To give you an example, I requested quotes for insurance for a seven-day trip to Canada that cost me $1,000. I received 24 quotes that ranged from $23 to $105.62 for the duration of my holiday. For an extra cost, I could add coverage for a range of optional extras, including sports equipment, electronics, and car rental collision.

More specialized coverage options are also available, including cruise insurance, senior travel insurance, annual travel insurance, and travel medical insurance. Again, the prices, terms, and features of these vary according to the details of your trip and the policy you choose.

TravelInsurance.com has a user-friendly online tool that enables you to find and compare travel insurance policies. It’s very easy to use, and you can have your policy and coverage documents in your inbox in as little as 10 minutes.

You begin by entering details about your trip. TravelInsurance.com will then recommend policies based on these details. You can select the one that’s best suited for your needs, pay for it immediately, and receive confirmation by email.

When it comes to claims, you don’t interact directly with TravelInsurance.com. Instead, you will have to make your claim through the policy provider you go with.

To get started with TravelInsurance.com, head to the company website and enter your trip details. The information you will need on hand includes your total trip cost, destination country, trip dates, age, and residence information.

Once you’ve filled this in, hit the “Get Quotes Now” button to see a list of insurance policies that fit your requirements. You can shortlist a few and compare them with the comparison tool, which clearly lists what is and isn’t included in each policy.

If you find one you like, you can hit the “Buy Now” button to purchase cover immediately. You will need to fill in your personal information and address, select which (if any) optional extras you require, and enter your payment details. Follow the prompts to complete the checkout, and your policy should be in your inbox within minutes.

I found this process to be very self-explanatory, and you shouldn’t have any issues. The user interface is clear and intuitive, and the company doesn’t use any misleading pricing techniques or make the checkout complicated.

The terms and fees of policies purchased through TravelInsurance.com vary according to the duration, destination, and cost of your trip. Prices can range from as little as $10 for short, cheap trips to hundreds or even thousands of dollars. Policy terms can range from a single day to 12 months or more.

TravelInsurance.com doesn’t have a mobile app.

TravelInsurance.com is a big player in the travel insurance industry, and it’s safe and reliable to use. It has a perfect five-star and A+ rating on the Better Business Bureau (BBB) website, where it has been accredited since 2012. What’s more, there have been only nine customer complaints in the past three years, and these have all been resolved.

On top of this, TravelInsurance.com has a rating of 4.6 out of 5 stars on Trustpilot, which is excellent for a company working in the insurance space. The company also clearly states that it uses various security measures, including encryption, to protect customer data.

TravelInsurance.com offers phone, ticket, and live chat support. Phone service is available from Monday to Friday, 9am-8pm (ET), and you should be able to chat with an agent immediately during these hours. Otherwise, you can submit a ticket. You’ll usually get a quick reply during business hours.

There are also loads of learning resources to help you understand more about travel insurance and what it includes. The blog contains a selection of informational articles, and there’s a decent FAQs page. There’s also step-by-step documentation to help you make a claim.

TravelInsurance.com is a comparison website designed to connect you with the most appropriate travel insurance policy for your needs. It works with various reliable travel insurance providers, and it offers policies for everything from short trips and cruises to annual travel cover.

What’s more, TravelInsurance.com enables you to purchase a policy directly through its website. This is very easy to do and normally takes just a few minutes. It has some of the most competitive prices I’ve seen, and it has great ratings across the internet.

All things considered, I’d seriously recommend giving TravelInsurance.com a go if you need a travel insurance policy of any type.

222 Broadway, 19th Floor, New York, NY, 10038

FAQs

FAQsDaniel Blechynden is an insurance writer at BestMoney.com, specializing in car insurance. He has contributed to numerous popular websites, drawing on his degrees in Chemistry and Marine Science from the University of Western Australia for rigor in research. Daniel’s background in technology and science informs his dependable reviews and financial insights.

Faye Travel Insurance is a new travel insurance provider, underwritten by United States Fire Insurance Company. It was built during the COVID-19 pandemic and launched in early 2022.

Claims processing is quick, and you can do this on Faye’s mobile app. The company offers fully customized plans to ensure you're not paying for features you don't need. What’s more, its 24-hour customer support means you can speak to real people (not robots!) throughout your travels.

Faye is a modern take on travel insurance. It’s a fully digital experience that allows you to purchase policies, file claims, and receive payouts through an app. The entire process is fast and secure, and you can receive reimbursement directly to your Faye Wallet, a secure digital debit card that you can add to Apple Wallet or Google Wallet, to then simply tap and pay.

Faye's tech-based approach makes it suitable for people who want something different from lengthy paperwork-based traditional insurance. It’s also ideal for frequent travelers who value convenience and want a plan that fits their exact needs. With Faye, you start with a base plan that you can customize with additional bundles, including rental car care, extreme sports protection, vacation rental damage protection, and “cancel for any reason” coverage.

Unlike other travel insurance providers, Faye doesn’t offer tiered plans. Instead, there is one base plan with the option to add additional riders such as pets, extreme sports, and medical coverage. The base package includes the following:

| Base plan | ||

|---|---|---|

|

| Maximum payout limit |

Medical cover | Medical evacuation and repatriation of remains benefit | Up to $500,000 |

Return transportation | Included | |

Transportation of child/children | Included | |

Transportation to join you | Included | |

Political or security evacuation and optional natural disaster evacuation | Up to $100,000 (international trips only) | |

Accident and sickness medical expense | Up to $250,000 for international trips ($50,000 for domestic) | |

Dental expense sublimit | Up to $750 | |

Cancellation and interruption | Trip cancellation | 100% of trip cost |

Trip interruption | 150% of trip cost | |

Trip delay | $300 per day, to a maximum of $4,500 | |

Travel inconvenience* | Baggage delay | $200 |

Delay at security check-in | $200 | |

Flight delay | $200 | |

Flight cancellation | $200 | |

Flight diversion | $200 | |

Rental property lockout | $200 | |

Hotel late arrival | $200 | |

Travel delay: internet usage fee | $50 | |

Travel delay: airline club admission fee | $25 | |

Baggage and personal effects** (Up to $2,000 per person per trip) | Baggage delay | $300 |

Passport, visa, or other travel documents replacement | $50 | |

Credit card charges and interest | $50 | |

Per article limit | $150 | |

Combined articles limit | $200 |

*Travel inconvenience: up to a maximum of $600

**Baggage and personal effects: up to a maximum of $750

For an additional cost, you can include “cancel for any reason’” coverage. You can also pay extra for adventure and extreme sports protection within your medical cover. Faye offers additional bundles for rental car protection and pet expenses, the details of which are below.

| Rental car bundle | |

|---|---|

Optional rental car damage and theft coverage | Up to $50,000 |

Optional travel inconvenience: Closed attractionsBeach closureRainy vacationRental vehicle breakdownCredit/debit card canceledVacation rental | $200 per inconvenience, up to a maximum of $600 |

| Pet parent bundle | |

|---|---|

Optional pet or service animal return | Up to $250 |

Optional pet kennel | Up to $250 |

Optional pet or service animal travel medical expense | Up to $2,500 |

Optional quarantine kenneling expense | Up to $2,500 |

The cost of your policy depends on your trip details and the state in which you live. Most international destinations cost a similar amount, and the duration of your trip does not usually impact the base plan cost. However, it will likely increase your estimated trip cost—which will increase the price.

I inquired about insurance for a two-week vacation in Italy for a Colorado resident. My trip insurance cost $114.50 for the base plan, based on an estimated trip cost of $1,000. The trip cost is the maximum amount Faye will reimburse me if my trip is canceled. For a trip costing $4,000, the base plan cost is $211.82. These figures are accurate as of March 2023.

I also had the option to include extras on top of my base plan. “Cancel for any reason” coverage costs an additional $20.35, and adventure and extreme sports protection costs $37.86. If I wanted to protect a rental car against accidental damage and theft, this would add $7.58 per day. Vacation rental cover comes to $17.04, and pet care adds another $25.36. The total policy cost for the same trip is now $338.81.

You can purchase Faye’s travel insurance directly through its website or mobile app. The process is designed to be as quick and straightforward as possible, with one comprehensive base plan and the option to purchase additional insurance bundles.

If you need to submit a claim, you can do it via the Faye mobile app or by email. You can use your app to keep track of the claim status and to see if it has been approved. If you qualify for a quick reimbursement, Faye will send money to your Faye Wallet, which you can access immediately. The app also allows you to transfer that money directly to your bank account. Faye aims to process all claims within 48 hours.

Faye also offers real-time travel updates and 24/7 customer service via the app. You can be notified of flight delays, gate changes, and other helpful information like which baggage carousel to go to when you arrive. Its customer service team is available to offer guidance and help with time-sensitive tasks, like finding an emergency doctor.

To get started, select the "Check Pricing" button on Faye’s website. You’ll need to provide details about your destination, your home address, the number of people traveling, and each traveler's name and date of birth.

You’re then taken to a policy details page which will outline what’s covered and options for additional protection, such as rental car cover and pet care. Once you’ve tailored your cover to your requirements, select the “Get Covered” button.

You can now pay via Google Pay or enter your card details to purchase your policy. After you’ve paid, Faye will send you an email containing the policy information.

You can also follow the same steps on Faye’s mobile app. Via the app you can also pay with Apple Pay. I found the process straightforward and quick, both online and via the app. The steps are easy to follow, and the information provided on the policy details page is clear and transparent.

Faye doesn't charge any administrative, arrangement, or amendment fees on its insurance products. If you cancel your travel insurance before starting your trip, you can receive a full refund up to 14 days after buying the coverage, as long as you haven’t already made a claim and as long as your trip hasn't started yet. Faye’s terms are set out in its Terms of Use document, available to read before you commit to purchasing.

Yes! Faye is a tech-driven app-based service and doesn’t just include an app as an afterthought like many insurance companies. The app is available for both Android and iOS, and you can use it to complete the whole process from initial pricing inquiry to making a claim.

Some of the most highly-praised features of the app include its 24/7 customer support chat. You’ll also get real-time travel alerts direct to your phone, for example, if your flight is delayed. What’s more, the app includes the Faye Wallet, a secure digital debit card that ensures fast reimbursement on claims and common travel inconveniences, like flight delays. It works with Apple or Google Pay, or you can transfer the funds to your bank account by tapping "Redeem" in the wallet.

Despite being a newcomer in the travel insurance industry, Faye has gained a good reputation among its customers and has an excellent score of 4.7 on Trustpilot. Multiple customer reviews praise its reliable customer service, user-friendly mobile app, and prompt notifications of flight delays and reimbursements.

Faye is a member of the United States Travel Insurance Association (USTIA), and its travel insurance coverages are underwritten by the United States Fire Insurance Company.

Faye prides itself on its excellent customer service. Its website and mobile app have a chat feature, and you’ll be able to talk to a real human rather than a robot. I used the chat function to ask Faye a question and got a friendly and informative response from one of its support team within a few minutes.

You can also contact Faye via phone on 833-240-7056 or email them at support@withfaye.com. The chat function, email queries, and phone lines are all staffed 24 hours a day, seven days a week. Phone calls are answered within five minutes and emails are responded to within 24 hours.

Faye’s website has a FAQs section and a blog, and you can also sign up for its newsletter and receive announcements, updates, and travel inspiration in your inbox.

Faye is a new player in the travel insurance market, aiming to revolutionize the industry, and my experience with the company has been very positive. Its friendly and helpful 24/7 customer service is available through the website and mobile app and ensured I was able to get my questions answered when I needed them.

The app also comes with features like real-time travel alerts and digital payment cards, which sets it apart from its competitors. The base plan and extra bundles cost less than many other insurers, making Faye a great choice for budget-conscious travelers.

Is Faye Travel Insurance legit?

Yes, Faye is a legitimate travel insurance company. It provides cover for medical expenses, trip cancellation and interruption, and other travel-related losses in accordance with its policy terms.

Is there a money-back guarantee?

Faye does not offer any money-back guarantees. However, it does offer a 100% refund if you cancel your policy within 14 days of purchase and have not made a claim.

What is the Faye Wallet?

The Faye Wallet is a digital payment card in the Faye app that allows quick reimbursement when making a claim. It works with Apple or Google Pay, or you can transfer the funds to your regular bank account by tapping “Redeem” in the wallet.

Emma Street is a finance writer at BestMoney.com specializing in debt consolidation and loans. With a BSc in Computer Science and over 15 years in software development, her experience in InsureTech and FinTech fuels her passion for exploring the intersection of technology and personal finance.

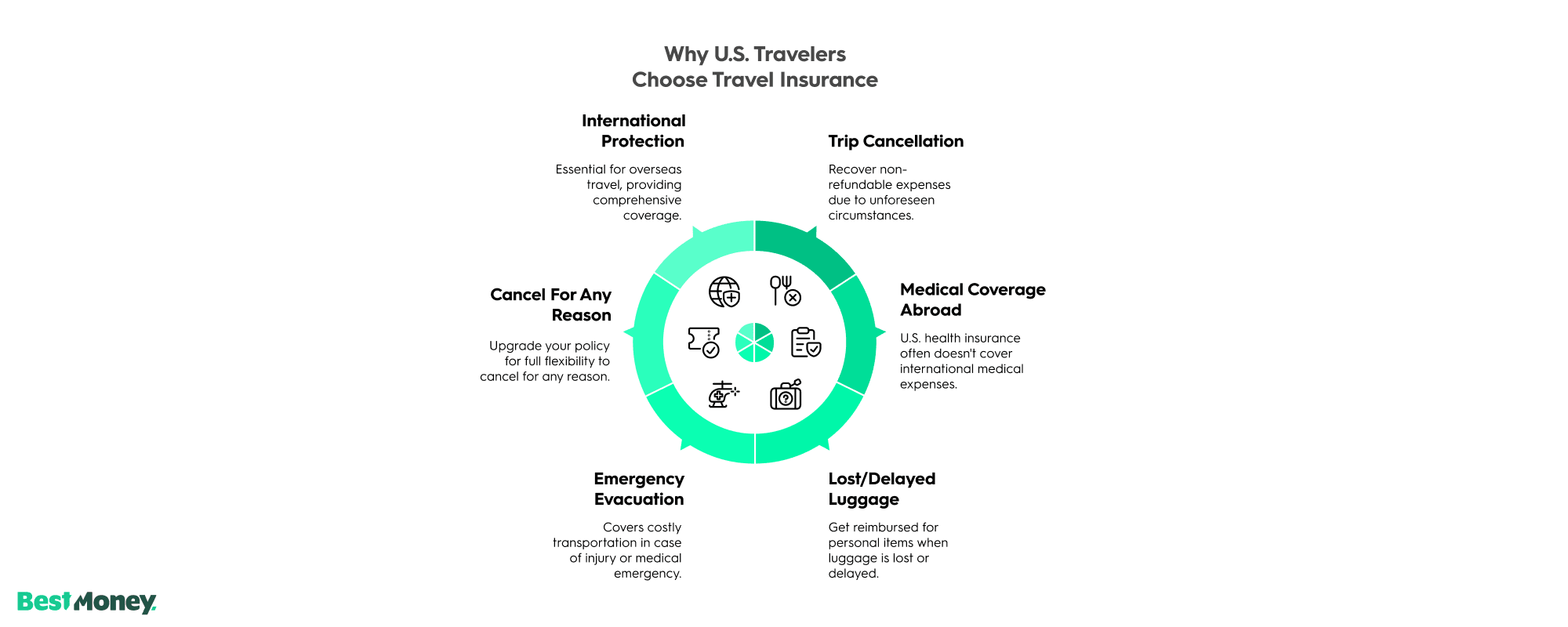

Travel insurance protects travelers by reimbursing or supporting them when trips go wrong—such as canceling prepaid travel, facing a medical emergency abroad, losing baggage, or needing an emergency evacuation. Whether you’re booking a domestic flight or searching for the best travel insurance international plan, having coverage in place provides peace of mind.

For overseas travel, your usual health plan may not apply, and that’s where international travel insurance becomes essential. Many individuals choose a travel insured international provider to ensure full support when far from home.

At BestMoney.com, we understand the importance of making informed financial decisions. Our team of financial experts and editors conducts thorough research across lending, banking, home loans, personal finance, and insurance to provide you with comprehensive comparisons and insights. We continuously update our content to reflect the latest market trends and offerings, ensuring you have access to current, reliable information.

We offer a wide range of services including detailed comparison tools and expert reviews, all designed to meet your specific financial needs. Our mission is to empower you to make confident, well-informed choices that help you achieve your financial goals.

Before purchasing a policy, it helps to review a travel insurance comparison of features and costs. Here are the main types of coverage to understand:

This protects you if you must cancel or cut short your trip due to illness, weather disruptions, or emergencies.

Covers loss, theft, or damage to your luggage and items while traveling

Pays for necessary medical care abroad such as hospital stays, doctor visits, and emergency treatment

Covers transportation to the nearest medical facility or back home in severe cases

Provides financial coverage in case of fatal or disabling incidents during your trip

| Customizable travel insurance |

Basic plans typically include 24/7 assistance, but optional upgrades provide broader protection:

| Quick quote for travel insurance |

Travel insurance usually costs between 4% and 10% of your total trip value.

Key pricing factors include:

Use travel insurance quotes tools or travel insurance comparison platforms to assess value versus cost and avoid overpaying for unnecessary add-ons.

Each has duration limits, so check how long each trip can be and whether destinations fall under coverage. Many travelers insurance providers offer both options with flexible terms.

Finding the best travel insurance requires more than a low price:

Travel insurance is more than a backup plan—it protects your investment, your health, and your peace of mind. From medical emergencies abroad to lost luggage or last-minute cancellations, here’s why smart travelers are choosing to get covered before they go.

You should consider a policy if:

Travel insurance is especially important if you're booking expensive tours, traveling with children or seniors, or visiting areas with political or health instability.

Not all policies cover pandemic-related cancellations or medical needs. However, many providers now include COVID-19 coverage under trip cancellation and medical insurance.

| Award-winning coverage |

Avoid these pitfalls when choosing travel insurance:

Taking time to research your plan ensures you get meaningful coverage when you need it most.

Pre-existing conditions are one of the most misunderstood areas of travel insurance. A pre-existing condition refers to any illness or medical issue you had before buying your policy. While many plans exclude coverage for these, there are ways to ensure protection:

Travelers with chronic illnesses, recent surgeries, or ongoing treatments should prioritize policies that allow for waivers or explicitly include medical history coverage.

Cancel for any reason (CFAR) insurance is an optional upgrade that provides maximum flexibility if your plans change unexpectedly. Unlike standard trip cancellation, which only reimburses for specific listed reasons like illness or death, CFAR allows broader cancellation options.

Travel delays and missed connections can disrupt your itinerary and lead to extra costs. Fortunately, many travel insurance plans offer compensation for these issues.

This is especially important for international travel insurance since missed layovers or rebookings can cost hundreds—or more—when abroad.

Filing a travel insurance claim can be straightforward if you gather the right documents. Keeping digital and physical copies ensures a smooth process:

Promptly filing with accurate information increases your chances of fast reimbursement. Travelers insurance providers often let you submit claims online or through mobile apps, streamlining the process