Our product scores consist of a combination of the following 3 components:

Popularity

BestMoney measures user engagement based on the number of clicks each listed brand received in the past 7 days. The number of clicks to each brand will be measured against other brands listed in the same query. Therefore, the higher the share of clicks a brand receives in any specific query, the higher the Click Trend Score. BestMoney accepts advertising compensation from companies, which impacts their (and/or their products’) position, and in some cases, may also affect their Click Trend Score.

Brand Reputation

Semrush is a trusted and comprehensive tool that offers insights about online visibility and performance. The BestMoney Total Score will consist of the brand's reputation from Semrush. The brand reputation is based on Semrush's analysis of clickstream data, which includes user behavior, search patterns, and engagement, to accurately measure each brand's prominence, credibility, and trustworthiness. If a brand does not have a Semrush score, the BestMoney Total Score will be based solely on the Click Trend Score and Products & Features Score (read below).

Features & Benefits

BestMoney’s editorial team researches and reviews financial products based on factors such as: range of products and services offered, ease-of-use, online accessibility, customer service, special awards, and more. Each brand is then given a score based on the offerings in each parameter. The specific parameters which we use to evaluate the score of each product can be found on its review page.

Travel insurance typically covers trip cancellations, medical emergencies, travel delays, lost baggage, and emergency evacuation, depending on the policy.

Does travel insurance cover medical expenses abroad?

Yes, most plans cover emergency medical treatment and hospitalization abroad, which is especially important since U.S. health insurance often doesn’t apply internationally.

What is not covered by travel insurance?

Travel insurance usually excludes pre-existing conditions (unless waived), risky activities, cancellations for non-covered reasons, and incidents involving alcohol or negligence.

How much travel insurance coverage do I need?

You should have enough coverage to match your total trip cost for cancellations and at least $50,000–$100,000 in medical coverage for international travel.

When should I buy travel insurance?

You should buy travel insurance soon after your first trip payment to maximize coverage options like pre-existing condition waivers and cancellation flexibility.

What Is Travel Insurance And Why It Matters

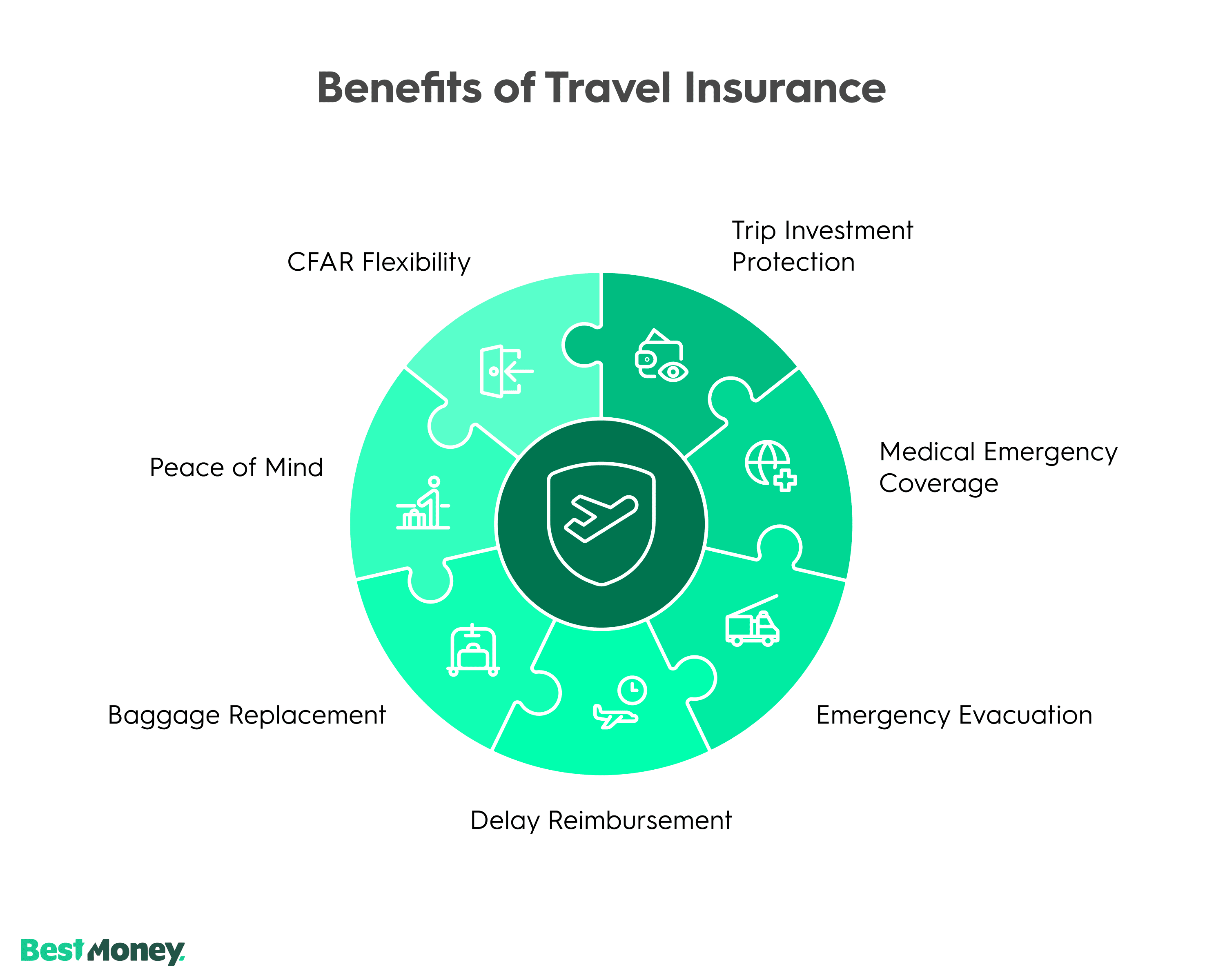

Travel insurance protects travelers by reimbursing or supporting them when trips go wrong, such as canceling prepaid travel, facing a medical emergency abroad, losing baggage, or needing an emergency evacuation. Whether you’re booking a domestic flight or searching for the best travel insurance for international travel, having coverage in place provides peace of mind.

For overseas travel, your usual health plan may not apply, and that’s where international traveler insurance becomes essential. Many individuals choose an international travel insurance provider to ensure full support when far from home.

U.S. travelers spent $5.56 billion on travel insurance in 2024, according to the U.S. Travel Insurance Association (USTIA). This was a 46% increase from 2019, which shows that travelers are increasingly prioritizing protection as an essential part of the travel planning process.

Traveler insurance protects your investment by covering cancellations, delays, lost baggage, and emergency medical expenses.

Medical and evacuation coverage are the most important benefits, especially for international travel.

Policies typically cost 4%–10% of your trip price, with age, destination, and trip length affecting premiums.

Buying within 14–21 days of booking unlocks stronger benefits, including pre-existing condition waivers and CFAR options.

The best provider balances coverage limits, claims reliability, and price—not just the lowest premium.

What Does Travel Insurance Cover?

Travel insurance covers financial losses and emergencies that can happen before or during your trip. Most comprehensive policies include the following protections:

Trip Cancellation, Interruption, And Delay

Trip cancellation: Reimburses prepaid, non-refundable costs if you cancel for a covered reason such as illness or severe weather.

Trip interruption: Covers unused expenses if your trip is cut short.

Trip delay: Pays for meals, lodging, and transportation if your travel is significantly delayed.

Cancel For Any Reason (CFAR): An optional upgrade that allows cancellation for broader reasons not covered by standard policies.

Baggage And Personal Effects

Lost, stolen, or damaged luggage: Covers the cost of replacing personal items if your baggage is lost, stolen, or damaged.

Airline filing requirement: You may need to file a claim with the airline first before your insurance coverage applies.

Emergency Medical Coverage

Emergency treatment abroad: Pays for hospital stays and emergency care if you get sick or injured while traveling.

Gap in U.S. health insurance: Especially important for international travel, where your domestic health plan may not apply.

Pre-existing conditions: May be excluded unless you purchase your policy within the required window and qualify for a waiver.

Emergency Evacuation And Repatriation

Emergency transport: Covers transportation to the nearest adequate medical facility or back home if you have a serious medical emergency.

"Adequate" defined by your insurer: Note that the facility your insurer selects may not meet your personal expectations—insurers determine adequacy by medical standard, not preference.

Cost without coverage: According to the CDC, medical evacuation costs range from $25,000 for transport within North America to over $250,000 for remote international locations.

Accidental Death And Flight Accident Coverage

Accidental death benefit: Provides a financial benefit to your beneficiaries in the event of a fatal accident during your trip.

Disabling injury benefit: Pays a benefit if you suffer a qualifying disabling injury while traveling.

Standard inclusion: This coverage is typically included in comprehensive travel insurance policies.

Travel insurance usually costs between 4% and 10% of your total trip value. Data from Squaremouth shows that the average cost of travel insurance in 2026 is $307 per policy, with an average trip length of 15 days. That said, your actual premium can vary depending on the following factors:

Destination: International travel insurance usually costs more.

Traveler age: Older travelers may pay more, especially for medical coverage.

Duration: Longer trips require more coverage.

Risk level: Adventure activities or high-cost trips increase premiums.

Use travel insurance quotes tools or travel insurance comparison platforms to assess value versus cost and avoid overpaying for unnecessary add-ons.

Expert Tip: Don’t Trade Coverage for Affordability

"I’ve seen people take the most affordable plan they can get on the internet to save money. They disregard medical boundaries or lose track of whether they have coverage for their health history. Many families end up with huge hospital bills due to this."

To choose the best travel insurance provider, compare coverage limits, exclusions, pricing, and claims reliability, not just the premium cost. The right provider should match your destination, trip cost, health needs, and overall risk level. The best travel insurance for international travel will also depend on these same factors below.

Coverage and exclusions: Review what each policy covers and excludes, paying close attention to medical maximums, evacuation limits, trip cancellation benefits, and any coverage caps that could limit a payout.

Age-based pricing and limits: If you're an older traveler, check whether the provider reduces benefits or charges significantly higher premiums based on age, as this varies widely across insurers. Best travel insurance for seniors may offer tailored support and higher medical limits

Claims reliability: Review customer feedback to understand how efficiently the provider processes and reimburses claims. A low premium means little if claims are slow or disputed.

Traveler profile and trip type: Compare travel insurance quotes based on whether you're traveling solo or with family, your destination, and the nature of your trip, since these factors affect both pricing and the coverage you actually need.

International travel priorities: For overseas trips, prioritize best travel insurance international providers with high medical limits, strong emergency evacuation coverage, and 24/7 assistance services.

Freely: Best for mobile-first travelers and customizable add-on coverage

Comparing Top Travel Insurance Providers

Provider

Medical & Evacuation Strength

Trip Cancellation & CFAR Options

Claims & User Experience

Faye

Comprehensive international medical coverage with emergency evacuation support

Includes trip cancellation with optional Cancel For Any Reason (CFAR‑style) upgrades on eligible plans

Fully digital claims process with app-based management and typically fast reimbursements

TravelInsurance.com

Varies by insurer (comparison platform with high-limit medical/evac plans)

Wide trip cancellation options; CFAR on select plans depending on provider.

Easy online comparison and purchase; claims handled directly by the selected insurer

Generali

Strong medical and evacuation coverage backed by global assistance services

Multiple plan tiers with trip cancellation; availability of optional upgrades (including CFAR)

Established claims system with phone and online support, plus 24/7 travel assistance

Allianz Travel Insurance

Global emergency medical and transportation benefits

Trip cancellation for covered reasons; optional “cancel anytime” upgrades on some plans

24/7 assistance and a structured online claims portal supported by phone and email channels

Squaremouth

Access to policies with high medical and evacuation limits

Extensive filtering for trip cancellation benefits; CFAR available on select plans

Transparent comparison tools and customer support; claims managed by the selected insurer

IMG

Robust international medical‑focused coverage with strong evacuation benefits

Trip cancellation coverage available on comprehensive plans, CFAR offered

Traditional online and phone-based claims support with broad international service

Travel Insured International

Comprehensive medical and evacuation protection across most trip protection plans

Strong trip cancellation benefits with flexible upgrades, including CFAR on select plan options

Multiple service channels, streamlined claims process, 24/7 assistance

Freely

Solid emergency medical coverage and evacuation for global travelers

Bundled trip cancellation; optional add-ons for extra cancellation and activities

Mobile‑first policy management with simplified, app‑based claims experience

Top Reasons Why U.S. Travelers Choose Travel Insurance

U.S. travelers choose travel insurance to protect their trip investment and avoid unexpected financial losses if plans change or emergencies arise.

Protect expensive trip investments: Recover prepaid, non-refundable travel costs if you must cancel or interrupt your trip.

Cover medical emergencies abroad: Pay for emergency medical care when your usual health insurance doesn’t apply overseas.

Pay for emergency evacuation: Covers costly transport to a hospital or back home due to serious illness or injury.

Reimburse for delays and missed connections: Compensation for extra costs from delayed flights or missed connections.

Replace or reimburse lost, stolen, or damaged baggage: Recoup expenses for lost or damaged luggage and personal items.

Peace of mind: Travel with less stress knowing you’re protected.

Cancel For Any Reason (CFAR) flexibility: Cancel for broader reasons and receive partial reimbursement.

What Add-Ons Are Available With Travel Insurance?

Basic plans typically include 24/7 assistance, but optional upgrades provide broader protection:

Extreme sports coverage for high-risk activities

Rental car damage and theft protection

Dental and vision emergency benefits

Cancel For Any Reason for full travel flexibility

Best travel insurance for seniors may offer tailored support and higher medical limits

Electronics or valuables coverage for items like laptops, cameras, or professional equipment.

Cruise trip add-on for cruise interruption and cabin confinement.

What Are Common Mistakes Travelers Make When Buying Insurance?

Avoid these pitfalls when choosing travel insurance:

Buying too late: Purchasing your policy more than 14 to 21 days after your first trip payment can disqualify you from key benefits, including pre-existing condition waivers and CFAR upgrades.

Relying on credit card coverage: Credit card travel insurance is typically limited in scope and rarely provides adequate protection for international medical emergencies or evacuation.

Skipping the exclusions: Failing to read your policy's exclusions is one of the most common reasons claims are denied. Know what is and is not covered before you travel.

Underestimating evacuation costs: Emergency evacuation and repatriation can cost tens of thousands of dollars. Skipping or undervaluing this coverage is a significant financial risk.

Not comparing quotes or benefit caps: The lowest-priced plan may carry coverage caps that limit your actual payout. Always compare limits alongside premiums.

Overlooking activity exclusions: Adventure sports, scuba diving, skiing, and similar activities are often excluded from standard policies and may require an additional rider or specialized plan.

Choosing price over medical limits: Selecting the cheapest plan without reviewing medical coverage limits can leave you seriously underinsured if an emergency occurs abroad.

Does Travel Insurance Cover Pre-Existing Medical Conditions?

Pre-existing conditions are one of the most misunderstood areas of travel insurance. A pre-existing condition refers to any illness or medical issue you had before buying your policy. While many plans exclude coverage for these, there are ways to ensure protection:

Some policies offer pre-existing condition waivers if you buy within 14 to 21 days of your first trip payment

This waiver allows coverage for medical treatment or trip cancellation due to known health issues

Best travel insurance for seniors often includes enhanced pre-existing condition options

Always read the definition of pre-existing condition in the policy—it may vary

Travelers with chronic illnesses, recent surgeries, or ongoing treatments should prioritize policies that allow waivers or explicitly include medical history coverage.

Expert Tip: Buy Early to Avoid Denial

"Having a chronic condition doesn't mean you can't get coverage. A pre-existing condition waiver can protect you, but timing matters. You'll typically need to purchase your policy shortly after making your first trip deposit. Buy early, and your insurer can't look back at your medical history to deny a future claim."

What Is CFAR (Travel Insurance Cancel For Any Reason) And When Should I Use It?

Travel insurance Cancel For Any Reason (CFAR) is an optional upgrade that provides maximum flexibility if your plans change unexpectedly. Unlike standard trip cancellation, which only reimburses for specific listed reasons, Cancel For Any Reason (CFAR) allows you to cancel for virtually any reason and still recover a portion of your costs.

Reimbursement range: Most Cancel For Any Reason (CFAR) policies refund between 50% and 75% of your prepaid, non-refundable trip costs, depending on the plan.

Cancellation window: You must cancel at least 48 to 72 hours before your scheduled departure to qualify for reimbursement.

Purchase timing: Cancel For Any Reason (CFAR) must be added within 14 to 21 days of your first trip payment. Waiting too long will disqualify you from this upgrade.

Best use cases: Cancel For Any Reason (CFAR) is particularly useful for travelers concerned about political unrest, evolving travel restrictions, or personal circumstances that may not qualify as a covered reason under a standard policy.

Trip complexity and cost: CFAR is worth considering for expensive or multi-destination trips where the financial risk of a last-minute cancellation is high.

How Does Travel Insurance Work With Trip Delays Or Missed Connections?

In 2025, 1.5 million flights were delayed, and over 100,000 flights were cancelled in the U.S. alone, according to the Bureau of Transportation Statistics. Without coverage, these disruptions can add high unplanned costs to your trip.

Delay coverage: If your flight is delayed due to weather, mechanical issues, or strikes, your policy may reimburse meals, lodging, and rebooking fees incurred during the delay.

Missed connections: Coverage typically applies when you miss a connecting flight due to a delay outside your control, such as a late inbound flight.

Minimum delay threshold: Most policies require a delay of six or more hours before benefits kick in. Check your policy's specific threshold before assuming you qualify.

Documentation required: You will need to submit supporting documentation to file a claim, including official airline delay notices and itemized receipts for any covered expenses.

International travel: Missed layovers and rebooking fees tend to be significantly more costly on international itineraries, making delay coverage especially valuable for overseas trips.

Many travelers insurance providers offer different terms, make sure to check with your provider when you buy your plan or before flying.

What Documents Do I Need To File A Travel Insurance Claim?

Filing a travel insurance claim is easier when you gather the right documents in advance. Most providers allow online or mobile app submissions, and filing promptly with accurate information increases your chances of fast reimbursement.

Original receipts: Keep itemized receipts for all covered expenses, including hotel stays, flights, and medical bills.

Proof of loss: Depending on your claim type, this may include police reports, official airline notices for delays or cancellations, or written confirmation of a covered event.

Physician's statement: For medical-related claims, your insurer will typically require a signed statement from the treating physician documenting your condition and treatment.

Trip cancellation or interruption documentation: Provide written evidence of the reason for cancellation or interruption, such as a death certificate, jury duty notice, or employer letter, where applicable.

Policy details: Have your full policy number and coverage summary on hand when submitting your claim to avoid processing delays.

What The Community Is Saying About Travel Insurance

Based on aggregated user reviews across travel forums and consumer platforms, travelers consistently say the best travel insurance depends on destination, trip cost, and health needs.

What Real Users Prioritize

Medical and evacuation coverage: Strong emergency medical and evacuation benefits are the most frequently cited priority, particularly among international travelers.

Claims reliability: Travelers consistently flag fast, hassle-free claims processing as a key factor in overall satisfaction with their provider.

Pre-existing condition coverage: Readers who purchase early emphasize the value of securing a pre-existing condition waiver, noting it significantly broadens their protection.

Annual plans: Frequent travelers recommend multi-trip annual plans as a cost-effective alternative to buying individual policies for each trip.

Policy clarity: Clear terms and minimal exclusions rank highly, with many reviewers citing confusing policy language as a source of frustration at claims time.

Many experienced travelers recommend buying coverage within 7 to 14 days of your first trip payment to qualify for the broadest range of benefits.

Bottom Line

Travel insurance protects your money and your health if something goes wrong before or during your trip. It can reimburse non-refundable expenses, cover emergency medical care abroad, pay for evacuation, and help with delays or lost baggage.

It’s especially valuable for international travel, expensive trips, and travelers with medical concerns. While not every trip requires coverage, travel insurance is often a smart investment when the financial risk of disruption is high.

The right policy balances cost, medical limits, cancellation protection, and reliable claims service—so you’re covered when it matters most.

Compare With BestMoney.com, Choose the Best for You

At BestMoney.com, we understand the importance of making informed financial decisions. Our team of financial experts and editors conducts thorough research across lending, banking, home loans, personal finance, and insurance to provide you with comprehensive comparisons and insights. We continuously update our content to reflect the latest market trends and offerings, ensuring you have access to current, reliable information.

We offer a wide range of services including detailed comparison tools and expert reviews, all designed to meet your specific financial needs. Our mission is to empower you to make confident, well-informed choices that help you achieve your financial goals.

Methodology: How We Evaluated Travel Insurance Providers

We evaluated travel insurance providers based on coverage depth, pricing transparency, claims reliability, and overall value for different traveler profiles. Our review process included:

Medical and evacuation limits: We compared emergency medical and evacuation coverage limits across providers, prioritizing those with high-limit options suited to international travel.

Cancellation and delay benefits: We analyzed trip cancellation, interruption, and delay benefits for each provider, including the availability and terms of optional Cancel For Any Reason (CFAR) upgrades.

Pre-existing condition waivers: We reviewed eligibility timelines and policy definitions for pre-existing condition waivers, noting differences in how providers define and apply these terms.

Price-to-coverage value: We compared sample quotes across different traveler ages and trip costs to assess how well each provider's pricing reflects the coverage offered.

Claims experience: We evaluated each provider's claims process, digital tools, and customer feedback trends to assess reliability and ease of use at claims time.

Insurer vs. marketplace distinction: We distinguished between direct insurers and comparison marketplaces, noting the differences in service model, claims handling, and policy selection.

We reviewed policy documents, insurer disclosures, pricing tools, and aggregated user feedback to identify providers offering strong protection, fair pricing, and reliable service.

Expert Insights by Christina Tunnah

Consider purchasing travel insurance soon after making your first trip deposit or payment, like booking a hotel or buying a flight. Timing can be important, as some benefits may only be available within a limited window after that initial expense.

Medical treatment and evacuation costs can vary significantly by destination, so it may be worth spending a few minutes researching healthcare costs at your destination when deciding on coverage limits.

Meeting the purchase window is only one part of the eligibility criteria when it comes to pre-existing medical condition waivers. You must also meet other conditions, such as being medically fit to travel when the policy is purchased.

CFAR benefits travelers who want greater control over their travel decisions and are willing to pay a bit more upfront for the option to cancel their trip for reasons that fall outside traditional coverage.

When it comes to illnesses while abroad, you’ll want to get medical reports and invoices from the doctors you see. Make sure the invoices are clear and have an address listed for verification purposes.

FAQs About Travel Insurance

Is travel insurance worth it?

Yes, travel insurance is worth it if you have prepaid non-refundable trip costs, are traveling internationally, or want protection against medical emergencies, cancellations, or travel delays. It can save you thousands of dollars if your trip is disrupted or you need emergency medical care abroad.

If your trip is inexpensive and fully refundable, you may not need coverage. But for costly or international travel, insurance is often a smart financial safeguard.

How does travel insurance work?

Travel insurance works by reimbursing you for covered losses or paying providers directly in certain emergencies. You purchase a policy before your trip, and if something goes wrong, such as a cancellation, medical emergency, or delay, you file a claim with documentation. If the issue is covered under your policy terms, the insurer reimburses you up to your coverage limits.

Can I add travel insurance after booking?

Yes, you can add travel insurance after booking your trip, as long as you buy it before departure. However, buying early, usually within 14 to 21 days of your first trip payment, may qualify you for additional benefits like pre-existing condition waivers or Cancel For Any Reason coverage. Waiting too long can limit your coverage options.

How do I get travel insurance?

You can get travel insurance by comparing quotes online through insurance providers or travel insurance comparison platforms. After selecting a plan, you purchase the policy and receive confirmation and policy documents immediately. To choose the right plan, consider your destination, trip cost, medical needs, and desired coverage limits before purchasing.

Best for: Fast digital claims and app-first travelers

Faye offers a single comprehensive policy with high coverage limits for baggage, personal belongings, medical emergencies, and evacuation. Its standout feature is a fully digital claims experience: submit your claim in the app, upload supporting documents, and receive reimbursement directly to your in-app wallet, often within 48 hours.

Pros:

Quick digital claims with fast reimbursement directly to your phone

Optional add-ons for pet care and vacation rental damage

Cons:

Premiums tend to run higher than some comparable policies

Why we chose it: Faye's 48-hour claims turnaround and app-based process make it one of the most streamlined options available for travelers who want a fast, low-friction claims experience.

Best for: Quick comparison shopping across multiple providers

TravelInsurance.com is a comparison marketplace that lets you review and buy policies from multiple travel insurance providers in one place. Instead of visiting individual insurers, you can enter your trip details and instantly compare coverage options, benefit limits, and prices side by side. Once you select a plan, coverage is provided and administered by the underlying insurance company, not the platform itself.

Pros:

Side-by-side policy comparisons across multiple insurers

24/7 international travel assistance included with listed plans

Cons:

Claims are handled by the individual insurer, not TravelInsurance.com, so the experience varies by provider

Why we chose it: TravelInsurance.com earns its spot for travelers who want to shop efficiently. Rather than researching insurers one by one, you get a consolidated view of coverage limits, benefits, and pricing in a single session, making it easier to find a policy that fits your trip without the legwork.

Best for: Full-service travel coverage with strong assistance support

Generali offers three plan tiers covering trip cancellations, medical emergencies, baggage loss, and travel delays, backed by 24/7 global assistance across 35-plus multilingual service centers. All plans include strong medical evacuation coverage, and claims can be submitted entirely online for easier tracking and documentation.

Pros:

Three plan tiers with broad coverage options, including sporting equipment and emergency dental

Strong medical evacuation limits across all plans

Cons:

Pre-existing condition coverage is only available on the highest-tier plan

Why we chose it: Generali stands out for the depth of its assistance network and the consistency of its evacuation coverage across all plan tiers. For travelers heading overseas, particularly to remote or higher-risk destinations, that combination of global support infrastructure and strong medical limits offers meaningful, reliable protection.